Business Loan In Singapore: 6 Tips To Increase Your Approval Chances

Does your business need a loan? Have you already tried applying for loans in the past but got rejected?

In Singapore, it’s almost impossible to go about building up your business without getting a business loan. Having your business loan rejected can be extremely troublesome.

If you have been following this space, we have previously discussed some possible reasons why your business loan might have been rejected. So, what can you do to ensure that your next application will go smoothly? How can you get your hands on funds as soon as possible to grow your business?

Here, we will be showing you some great ways to increase your chances of getting your business loan approved.

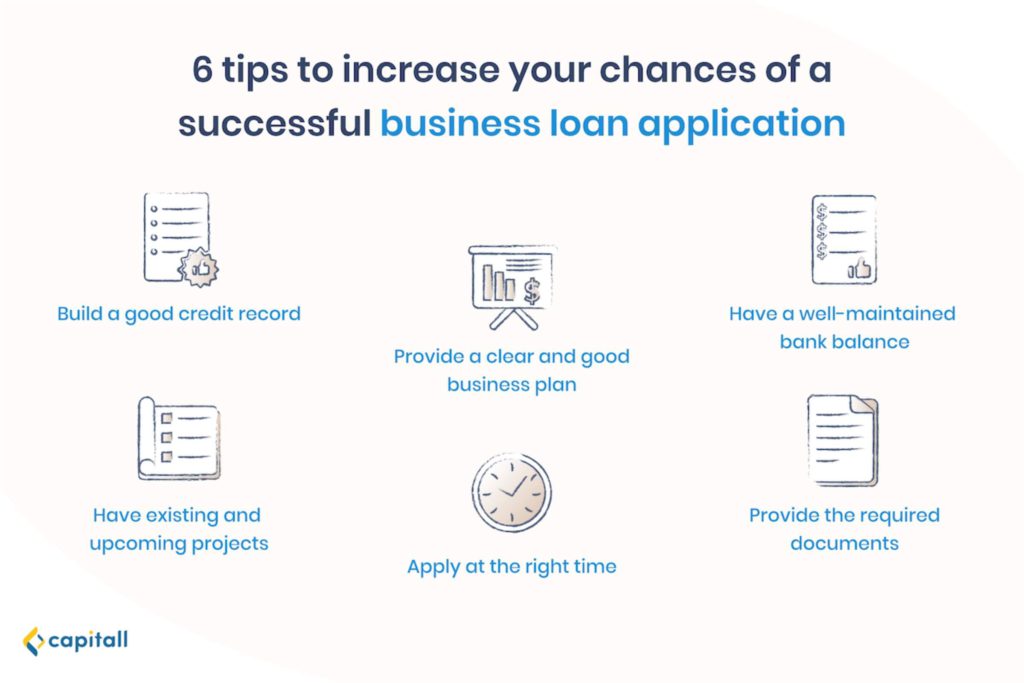

1. Build A Good Credit Record

Having a strong credit record is of paramount importance. Whether you’re borrowing from banks or private financial institutions, having a good credit history will definitely be helpful for you.

Businesses with good credit scores signal to lenders and banks that they are responsible and can make timely payment.

After all, nobody likes lending out funds to someone who cannot be trusted to repay on time.

Showing banks and lenders that you are a good steward of their resources signals to them that they are taking a lower risk when they are lending funds to you.

On the other hand, having a poor record induces low confidence and potentially causes your loan application to be rejected.

2. Provide A Clear And Good Business Plan

Imagine lending some funds to a friend.

Would you rather lend it to him if he provided a good reason for why he needs the funds? Or would you lend it to someone who is secretive about what they want to use the funds for?

The same applies for getting yourself a business loan.

Having a clear business plan is key in getting your loan application approved because it signals to banks and private financial institutions that your business is trustworthy.

Besides telling them how their funds will be utilised, you should also explain how you intend to repay the debt. Giving the impression that you know how to use the borrowed funds wisely will enable your application to be approved quickly.

With Capitall, you can secure up to S$300,000 to expand your financial prospects.

3. Having A Well-maintained Bank Balance

This might sound a little too simple. But having a healthy bank balance is a great way to increase your loan application’s approval chances.

This is because a well-maintained bank balance shows that your business is doing reasonably well and not in some kind of dire financial situation.

Keeping your bank balance in a healthy state shows banks and private financial institutions that you have the ability to repay loans and not default on your payments.

4. Have Existing And Upcoming Projects In The Pipeline

Another great way to show that your business is a good prospect to lend loans to is to have ongoing projects.

Showing to lenders and banks that you have projects on a regular basis tells them that your business is doing well. After all, no one wants to lend a huge sum to a fumbling business that has little to no chances of repaying debt.

Having projects on your plate shows that your company is doing well and is able to generate income to pay back the loans.

5. Apply At The Right Time

Yes — there is a “right time” and a “wrong time” to apply for loans. When your business is volatile and unstable, applying for loans becomes much harder.

Firstly, unstable businesses tend to not have the best bank balances.

Secondly, they tend to have few or no projects in the pipeline. These signal to lenders that they might be taking a higher risk lending funds to such businesses.

So how do you go about applying for loans when you need one?

One way is to secure funding early, even if you don’t need the funds immediately. It’s always easier to secure loans when your business is doing well. Hence, being able to make projections on when you need funds ahead of time is crucial.

Since businesses tend to be seasonal, most private financial institutions require the last 6 months of bank statements when you’re applying for a loan.

Keeping this in mind, it’s definitely wiser to apply for loans when your business is doing well, even if you don’t need it urgently at the moment.

6. Provide The Required Documents

When applying for loans, having the necessary documents ready definitely helps. You don’t want to be scrambling to get your documents and not know what is required of you.

This causes you to miss out on submitting important documents and also gives lenders the impression that you are uncertain.

Here are some of the documents you’ll need when applying for a business loan.

Do note that the documents required may differ depending on lenders:

- ACRA Business Profile Information

- Latest 6 months of bank statements

- Company financial statements for the past year

- Latest Credit Bureau Singapore (CBS) credit report of applicant(s)

- Latest Moneylenders Credit Bureau (MLCB) report of applicant(s)

- Upcoming contracts

Optional documents:

- Aging reports

- Expected invoices

- Other documents that may be applicable to the loan assessment

1. ACRA Business Profile Information

Your business profile information from the Accounting and Corporate Regulatory Authority (ACRA) will allow private financial institutions and banks to have an overview of your business.

In it, the document will contain information about your shareholders, directors, and your company’s paid up capital. As such, financiers can understand the nature of your business and decide who to bring in as a guarantor if necessary.

2. Latest 6 Months Of Bank Statements

The last 6 months of bank statements will be needed by most financiers when you want to take a loan. This is because it can help them have a clearer picture of how your business is doing financially and help them decide if they are taking high risks lending funds to you.

3. Company Financial Statement For The Past Year

Your company’s financial statement for the past year serves a similar purpose as the bank statements. However, beyond just showing how well your business is doing, your financial statements show how consistent your business is with payments and repayments. It also serves as a track record of your business’ financial health.

4. Latest Credit Bureau Singapore (CBS) Credit Report Of Applicant(s)

The CBS Credit Report is a document which covers your credit score. Generally, lenders will require a business credit report from CBS to show that you have a healthy credit history.

5. Latest Moneylenders Credit Bureau (MLCB) Report Of Applicant(s)

The MLCB report is similar to the CBS credit report.

The main difference lies in that this document is required by private financial institutions.

Similar to banks, they will need you to show that your business has a healthy credit history before they can approve your business loan.

6. Any Upcoming Contracts, Aging Reports, Expected Invoices And Other Documents That May Be Applicable To The Loan Assessment

Other than showing that your business has regular projects and income, there are many ways to increase the approval of your application.

You can also submit expected invoices, upcoming contracts, or any other related documents to show that your company is doing well and has the capabilities to repay the loans.

Getting Your Business Loan Approved Is Not As Difficult As You Might Think

If your application was turned down before, it’s important to first consider the reasons why. Was it due to bad credit? Or was it due to incomplete information about your business?

If you’ve yet to apply for a business loan, you might want to check out the things to ask before getting a business loan in Singapore.

When applying for loans, earning trust from banks and private financial institutions is crucial. It’s not enough to just make claims about your businesses — you’ll need to show that your business is in good shape with the relevant documents.